☆ 조세저항주의자의 비참한 최후 ☆

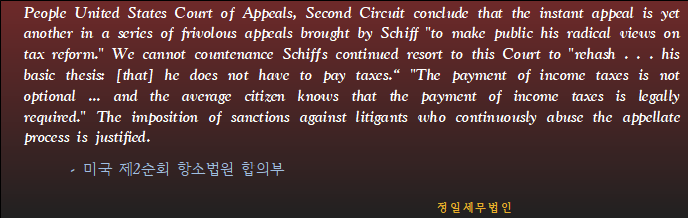

제2순회 항소법원은 즉흥적인 항소가 "조세 개혁에 대한 항소인(Irwin A.

Schiff)의 과격한 견해를 공표하기 위해" 그가 제기한 일련의 경솔한 항소의

또 다른 형태라고 결론을 내린다

법원은 쉬프(Irwin A. Schiff)가 "그는 세금을 낼 필요가 없다"(he does not

have to pay taxes)는 그의 기본 논제를 재탕하기 위해 이 법원에 계속 소송을

제기하는 것을 지지할 수 없다.

"소득세 납부는 선택 사항이 아니다... 그리고 일반 시민은 소득세 납부가

법적으로 요구된다는 것을 알고 있다."

항소 절차를 지속적으로 남용하는 소송 당사자에 대한 제재(벌금) 부과는

정당하다.

- 미국 제2순회 항소법원 합의부

· Wilfred Feinberg(1920~2014) 미국 제2순회 항소법원 판사(1966~1980),

수석판사(1980~1988) 및 법원장(1988~2014), 뉴욕 남부지방법원 판사

(1961~1966)

· William Homer Timbers(1915~1994) 미국 제2순회 항소법원 판사

(1971~1981) 및 법원장(1981~1994), 코네티컷 지방법원 판사(1960~1964)

및 수석판사(1964~1971)

· Roger Jeffrey Miner(1934~2012) 미국 제2순회 항소법원 판사(1985~1997)

및 법원장(1997~2012), 뉴욕 북부지방법원 판사(1981~1985)

출처 : 미국 제2순회 항소법원 1990.11.21. 선고 Schiff v. United States,

919 F.2d 830, 832 (2d Cir. 1990)

<해설>

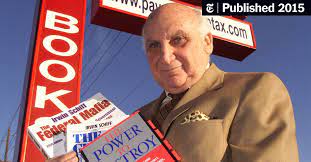

이 사건에서 ‘현대 조세 저항운동의 할아버지’(the grandfather of the

contemporary tax protester movement)로 미국의 대표적인 조세 거부주의자인

어윈 쉬프(Irwin Allen Schiff)는 1977년과 1978년 과세연도의 정상적인 세금

신고서를 제출하지 아니하고, 1977년 4월 1976년 과세연도에 대하여 변칙적인

신고서식 1040을 국세청(IRS)에 제출했다. 그 1040서식에는 쉬프(Schiff)의 이름,

주소 및 사회보장번호는 기재되어 있으나, 신고서에서 가장 중요한 소득금액등

재무 정보를 지재하지 않고, 대신 ‘별표에 기재함’이라고 표시하고 여백에

“이 신고서와 나에게 적용될 수 있는 법률을 이해하지 못합니다. 특정 질문은 미국

수정헌법 제4조와 수정헌법 제5조에 의거하여 특정 반대가 제기되었음을 의미

합니다.” 라고 기재했다.

신고서식 2페이지에서 쉬프(Schiff)는 ‘별표에 기재함’이라고 표시하고 하단에

“이는 미국 수정헌법 제4조와 수정헌법 제5조를 근거로 특정 질문에 대한 특정

반대가 제기됨을 의미합니다.” 라고 기재하여 부당한 조세저항 의지를 다시 한번

보여주었다.

쉬프(Schiff)는 1040서식에 국세청장에게 보내는 편지를 첨부했다. 그 편지에는

그가 받은 연방 준비금 지폐는 금이나 은으로는 교환할 수 없기 때문에 가치가

없다고 명시하고, "납세자는 소득세 신고서를 제출할 필요가 있다는 법적 근거가

없다.” 는 주장을 했다.

1982.12.2. 국세청은 쉬프(Schiff)에 대한 1976년부터 1978년까지의 기간에 대한

추징세액, 이자 및 벌금에 과세결정통지서를 발부하자 조세법원에 불복청구했으나

조세법원은 국세청의 과세처분을 지지했다.

제2순회 항소법원은 쉬프(Schiff)의 모든 주장이 전혀 가치가 없다고 판시했다.

첫째로 의회에 의해 유효하게 제정된 소득세의 부과가 헌법의 과세조항을 위반

한다는 쉬프(Schiff)의 주장은 이미 이전의 다른 소송에서 거부되었다.

둘째로 쉬프(Schiff)는 국세청의 과세 및 징수가 정당한 절차 없이 재산을 취득한

것에 해당한다고 주장했으나, 과세결정통지서에서 그가 조세법원에 항소할 권리가

있음을 분명히 알려 주었기 때문에 쉬프(Schiff)의 적법 절차 주장도 경솔한 것으로

판단했다.

또한 항소법원은 쉬프(Schiff)가 법원에 조세제도를 공격하는 경솔한 소송을 여러

차례 제기했으나 법원에서 모두 거부되었다는 사실을 언급하면서, 쉬프(Schiff)에게

2배의 비용과 $5,000의 손해 배상금을 미국 정부에 납부하도록 명령했다.

2006.2.24. 네바다 주 라스베이거스의 연방 지방법원은 조세 거부주의자

쉬프(Schiff)에게 세금 사기 혐의로 151개월의 징역형과 법정 모독죄로 추가

12개월(2012.9.21. 11개월로 1개월 단축)의 징역형을 선고했다.

또한 쉬프(Schiff)는 손해 배상금으로 420만 달러 이상을 납부하고 3년간 감독부

석방하라는 명령을 받았다. 이것은 쉬프(Schiff)가 연방 조세법 위반으로 유죄

판결을 받은 세 번째 사례이다.[결국 쉬프(Schiff)는 2015.10.16. 교도소 수감중

사망함]

이에 앞서 2005년 10월, 쉬프(Schiff)는 미국을 사취하고, 허위 소득세 신고서

준비를 돕고, 자신의 허위 세금 신고서를 제출하고, 수백만 달러의 체납 세금을

회피한 혐의로 유죄 판결을 받았으며, 그 이전에도 쉬프(Schiff)는 세금 범죄로 4년

이상을 감옥에서 보냈다.

쉬프(Schiff)는 이 사건을 포함하여 33년 동안 17건의 조세관련 소송을 제기하였

지만(별표 1 참조), 주장하는 내용이 “미국 조세법원은 독자적인 관할권이 없으며,

조세법원은 법률상의 법원이 아니라 IRS의 일부 조직이다.” 라고 주장하는 등 경솔

하고 증거도 없이 터무니 없는 주장으로 일관했기 때문에(별표 2참조), 법원은

한결같이 쉬프(Schiff)의 주장을 무효로 판결하거나 받아들이지 않았다.

이 사건에서 쉬프(Schiff)의 공범으로 기소된 전 여자친구인 신시아 넌(Cynthia

Neun)은 다른 사람들에게 소득세를 내도록 요구하는 연방 법령이 없다고 조언한

혐의로 68개월의 징역형과 110만 달러의 손해배상금 납부명령을 받았으며, 세 번째

공범인 로렌스 코헨(Lawrence Cohen)은 사기성 세금 신고를 도와준 혐의로

33개월의 징역형을 선고 받았으나, 소송이 확정되기전 2009.8.6. 사망했다.

IRS 범죄 수사 책임자 에일린 메이어(Eileen Mayer)는 "납세자는 자신의 납세

의무에 대해 이의를 제기할 권리가 있지만, 그러나 법을 위반할 권리는 없다."

(Taxpayers have the right to contest their tax liability; they do not

have the right to violate the law) 라고 말한 것처럼, 모든 시민은 우리 모두

에게 적용되는 법을 준수해야 한다.

|

[ 별표 1 ] 어윈 쉬프(Irwin Allen Schiff)가 제기한 조세소송 경력

① 미국 제2순회 항소법원 1979.12.12. United States v. Schiff, 612 F.2d 73

(2d Cir. 1979)

② 미국 재2순회 항소법원 1981. United States v. Schiff, 647 F.2d 163(2d Cir.

1981)

③ 미국 제2순회 항소법원 1984.12.20. Schiff v. Commissioner, 751 F.2d 116

(2d Cir. 1984) : 2배의 비용과 $2,500의 손해 배상금 지급명령

④ 미국 제2순회 항소법원 1985.12.31. Irwin Schiff v. Simon Schuster, 780 F.2d

210 (1985) : Irwin Schiff의 세금체납으로 국세청이 채권자인 SIMON &

SCHUSTER의 거래대금 압류하여 세금으로 충당하자, Irwin Schiff는

채권자를 상대로 소송을 제기했으나 기각됨

⑤ 미국 제2순회 항소법원 1986.9.15. United States v. Schiff, 801 F.2d 108

(2d Cir. 1986)

⑥ 미국 연방대법원 1987.3.30. United States v. Schiff, 480 US 945 (1987)

⑦ 미국 제2순회 항소법원 1989.5.17. United States v. Schiff, 876 F.2d 272(1989)

: 지방법원의 탈세 유죄판결과 보호관찰 조건에 대한 항소 기각

⑧ 미국 제2순회 항소법원 1990.11.21. Schiff v. Commissioner, 919 F.2d 830

(2d Cir. 1990) : 2배의 비용과 $5,000 손해 배상금 지급명령

⑨ 미국 조세법원 1992.3.26. Schiff v. Commissioner No. 33278-86 (U.S.T.C.

1992) : $25,000의 벌금 부과

⑩ 미국 네바다 지방법원 2003.6.16. United States v. Schiff, 269 F. Supp. 2d

1262 (D. Nev. 2003)

⑪ 미국 제9순회 항소법원 2004.8.9. United States v. Schiff, 379 F.3d 621

(9th Cir. 2004)

: 지방법원의 탈세 계획 조직, 마케팅 또는 홍보 사업에 대한 금지명령에 대한

항소 기각

⑫ 미국 네바다 지방법원 2006.2.24. United States v. Schiff, case no. 2:04 -cr-

00119–KJD-LRL(2006)

⑬ 미국 제9순회 항소법원 2007.12.26. United States v. Schiff, 2008-1 U.S.

Tax Cas. (CCH) paragr. 50,111 (9th Cir. 2007)

⑭ 미국 제9순회 항소법원 2010.6.11. U.S. v. Schiff, 383 F. App'x 649 (9th Cir.

2010)

⑮ 미국 연방대법원 2010.11.1. 선고 Schiff v. United States,131 S. Ct.532(2010)

⑯ 미국 네바다 지방법원 2012.9.21. United States v. Schiff, Case No. 2:04-CR-

00119-1 -KJD (D. Nev., 2012)

: 공모 및 세금 사기 혐의로 151개월의 징역형 선고 및 3년의 감독부 석방의 확정

재판 중에 15건의 법원 모독죄로 11개월의 징역형 추가 선고 확정

법원에 420만 달러의 손해 배상금 납부 명령 확정

⑰ 미국 제9순회 항소법원 2013.11.7. United States v. Schiff, 544 F. App'x 729

(9th Cir. 2013)

|

|

[ 별표 2 ] 어윈 쉬프(Irwin Allen Schiff)가 수년에 걸쳐 제기한 주장들

① 국세청은 소득세를 시행할 때 미국 헌법의 과세 조항에 의해 승인되지 않은 세금을

부과하려고 시도한다.

② 연방 소득세의 법적 결함은 부과가 이루어질 때까지 존재할 수 없다.

③ 소득세 신고는 자발적이며 "자발적 준수"(voluntary compliance)는 IRS가 대중을

오도하기 위해 사용하는 오해의 소지가 있는 문구이다.

④ 자발적으로 세금 신고서를 제출하지 않으면 세금 부과 할 수 없다.

⑤ 미국 조세법원은 독자적인 관할권이 없다. 그리고 조세법원은 법률상의 법원이

아니라 IRS의 일부 조직이다.

⑥ 법원의 판결과 법령에 따라 적절하게 정의된 "소득"(income)의 개념은 임금

(not wages)이 아니라 기업의 이익 뿐(only corporate profits)이다.

|