☆ 한국 법인세율 OECD 국가 중 10번째로 높다 ☆

1980년 이후 전 세계적으로 각 국가들은 높은 법인세율이 기업의 투자결정에

미치는 영향을 의식하여 법인세율의 인하에 초점을 맞추고 있다.

OECD 경제학자들이 발표한 매우 중요한 2008년 보고서에서 서로 다른

세금과 경제 성장 사이의 관계를 측정한 결과 법인세가 장기 경제성장에 가장

유해한 세금이며 높은 개인소득세가 뒤따른다고 밝혔으며, 소비세와 재산세는

상대적으로 덜 해로운 것으로 간주되었다. 실제로 이 보고서에서 법정

법인세율을 낮추면 "활기넘치고 수익성이 높은 기업, 즉 GDP 성장에 가장 큰

기여를 할 수 있는 기업에서 특히 큰 생산성 향상을 가져올 수 있다" 라고 밝혔다.

(OECD Economics Working Paper No. 620., 2008.7.11., 9p)

이러한 추세에 맞추어 OECD 국가 중 2010년 이후 법인세율이 인하된 국가는

39개국 중 23개국이며, 법인세율이 인상된 국가는 8개국(한국, 칠레, 포르투갈,

이탈리아, 터키, 슬로바키아, 아이슬란드, 라트비아)이다.

2010년 이후 법인세율이 변동되지 않은 국가는 8개국(멕시코, 호주,

오스트리아, 그리스, 체코, 폴란드, 아일랜드, 리투아니아)이다.

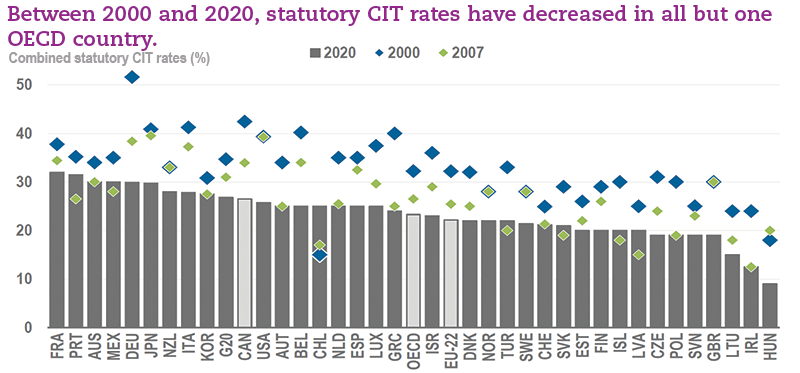

2020년 프랑스의 법인세율이 32%로 2010년 34.43%(3위)에서 2.43%p 인하

되었음에도 컬럼비아와 함께 OECD국가 중 가장 높은 국가에 속한다.

2000년 이후 OECD국가 중 유일하게 칠레만 계속 법인세율이 인상되었으며

나머지 38개국은 인하되었다.

미국과 일본은 2000년 이후 10년 동안 법인세율을 그대로 유지하였으나,

독일은 세계적인 세율 인하 추세에 맞추어 다른 어떤 국가보다도 대폭 인하

하였다.

미국은 2010년 법인세율이 39.2%로 OECD 순위 2위였으나, 2017년 세제

개혁으로 세율이 25.8%로 대폭 인하되어, 2020년 OECD 순위에서 한국보다

더 낮은 12위로 떨어졌다.

일본은 2000년 법인세율이 40.87%로 3위로 높은 국가였으나 그 이후 10년간

큰 변동이 없었으나 2020년에 29.7%로 7위로 떨어졌다.

독일은 2000년 법인세율이 52%로 가장 높은 국가였으나 그 이후 22.1%

포인트를 내려 2020년에 29.9%로 6위로 떨어졌다.

캐나다 역시 2000년 법인세율이 OECD 순위 2위인 42.57%로 높은

국가였으나 2020년에 26.5%로 인하되어 11위로 떨어졌다. 캐나다 정부는 주요

G-7 국가 중 가장 낮은 법인세율을 목표로 설정하고, 지난 20년 동안

캐나다는 16.07% 포인트를 인하하여 OECD 순위에서 9계단 하락했다.

한국의 법인세율은 2000년에 30.8%로 23위, 2010년에는 24.2%로 25위로

중위권에 머물렀으나, 2020년 현재 27.5%로 OECD 39개국 중 10위로 높은

편이다.

OECD는 “법정 법인세율의 대폭적인 인하에도 불구하고 법인세 수입은

GDP 성장과 수입 증가에 보조를 맞추거나 오히려 초과한 경우도 있다고

밝혔다.(“Fundamental Reform of Corporate Income Tax,” Organization for

Economic Cooperation and Development, OECD Tax Policy Studies No. 16., 2007)

[OECD 국가의 법인세율]

(%)

|

국가별 |

2020년 |

2010년 |

2000년 |

세율의 변화 |

|

세율 |

순위 |

세율 |

순위 |

세율 |

순위 |

2020년과 2010년 차이 |

2020년과 2000년 차이 |

|

프랑스 |

32.0 |

1 |

34.43 |

3 |

37.76 |

7 |

- 2.43 |

5.76 |

|

컬럼비아 |

32.0 |

1 |

33.0 |

5 |

35.0 |

12 |

1.0 |

3.0 |

|

포르투갈 |

31.5 |

3 |

26.5 |

17 |

35.2 |

11 |

+ 5.0 |

3.7 |

|

멕시코 |

30.0 |

4 |

30.0 |

7 |

35.0 |

12 |

0 |

5.0 |

|

호주 |

30.0 |

4 |

30.0 |

7 |

34.0 |

16 |

0 |

4.0 |

|

독일 |

29.9 |

6 |

30.2 |

6 |

52.0 |

1 |

0.3 |

22.1 |

|

일본 |

29.7 |

7 |

39.54 |

1 |

40.87 |

3 |

9.84 |

11.17 |

|

뉴질랜드 |

28.0 |

8 |

30.0 |

7 |

33.0 |

18 |

2.0 |

5.0 |

|

이탈리아 |

27,8 |

9 |

27.5 |

16 |

37.0 |

9 |

+ 0.3 |

9.2 |

|

대한민국 |

27.5 |

10 |

24.2 |

25 |

30.8 |

23 |

+ 3.3 |

3.3 |

|

캐나다 |

26.5 |

11 |

29.52 |

11 |

42.57 |

2 |

3.02 |

16.07 |

|

미국 |

25.8 |

12 |

39.2 |

2 |

39.3 |

6 |

13.4 |

13.5 |

|

벨기에 |

25.0 |

13 |

33.99 |

4 |

40.2 |

4 |

8.99 |

15.2 |

|

스페인 |

25.0 |

13 |

30.0 |

7 |

35.0 |

12 |

5.0 |

10.0 |

|

네덜란드 |

25.0 |

13 |

25.5 |

20 |

35.0 |

12 |

0.5 |

10.0 |

|

오스트리아 |

25.0 |

13 |

25.0 |

21 |

34.0 |

16 |

0 |

- 9.0 |

|

칠레 |

25.0 |

13 |

17.0 |

35 |

15.0 |

39 |

+ 8.0 |

+ 10.0 |

|

룩셈부르크 |

24.9 |

18 |

28.59 |

12 |

37.45 |

8 |

3.69 |

12.55 |

|

그리스 |

24.0 |

19 |

24.0 |

26 |

40.0 |

5 |

0 |

16.0 |

|

이스라엘 |

23.0 |

20 |

25.0 |

21 |

36.0 |

10 |

2.0 |

13.0 |

|

노르웨이 |

22.0 |

21 |

28.0 |

13 |

28.0 |

29 |

- 6.0 |

6.0 |

|

덴마크 |

22.0 |

21 |

25.0 |

21 |

32.0 |

20 |

3.0 |

10.0 |

|

터키 |

22.0 |

21 |

20.0 |

29 |

33.0 |

18 |

+ 2.0 |

11.0 |

|

덴마크 |

22.0 |

21 |

25.0 |

21 |

32.0 |

20 |

3.0 |

10.0 |

|

노르웨이 |

22.0 |

21 |

28.0 |

13 |

28.0 |

29 |

6.0 |

6.0 |

|

스웨덴 |

21.4 |

26 |

26.3 |

18 |

28.0 |

29 |

4.9 |

6.6 |

|

스위스 |

21.1 |

27 |

21.17 |

27 |

24.93 |

35 |

0.07 |

3.83 |

|

슬로바키아 |

21.0 |

28 |

19.0 |

31 |

29.0 |

27 |

+ 2.0 |

8.0 |

|

핀란드 |

20.0 |

29 |

26.0 |

19 |

29.0 |

27 |

- 6.0 |

9.0 |

|

아이슬란드 |

20.0 |

29 |

15.0 |

36 |

30.0 |

24 |

+ 5.0 |

10.0 |

|

에스토니아 |

20.0 |

29 |

21.0 |

28 |

26.0 |

32 |

1.0 |

6.0 |

|

라트비아 |

20.0 |

29 |

15.0 |

36 |

25.0 |

33 |

+ 5.0 |

5.0 |

|

체코 |

19.0 |

33 |

19.0 |

31 |

31.0 |

22 |

0 |

12.0 |

|

슬로베니아 |

19.0 |

33 |

20.0 |

29 |

25.0 |

33 |

- 1.0 |

6.0 |

|

폴란드 |

19.0 |

33 |

19.0 |

31 |

30.0 |

24 |

0 |

11.0 |

|

영국 |

19.0 |

33 |

28.0 |

13 |

30.0 |

24 |

9.0 |

11.0 |

|

리투아니아 |

15.0 |

37 |

15.0 |

36 |

24.0 |

36 |

0 |

9.0 |

|

아일랜드 |

12.5 |

38 |

12.5 |

39 |

24.0 |

36 |

0 |

11.5 |

|

헝가리 |

9.0 |

39 |

19.0 |

31 |

18.0 |

38 |

10.0 |

9.0 |

출처 : OECD.Stat “Statutory Corporate Income Tax Rates”